This short article represents the personal views of Cru World Wine CEO Jeremy Howard. It does not represent the view of the company or any of its representatives.

The Bordeaux 2023 en primeur campaign kicked off three weeks ago. As we approach the halfway point , what have we learned thus far?

Four main lessons seem to have emerged:

- The Bordelais are (mostly!) still serious about en primeur.

- If wines are priced appropriately, there is still robust demand from collectors to buy en primeur.

- The fine wine market takes into account back vintage pricing more than some châteaux would like to believe.

- A wine's average critic score is the most important determinant of price, more than château classification or reputation.

Bordeaux is still serious about making en primeur work

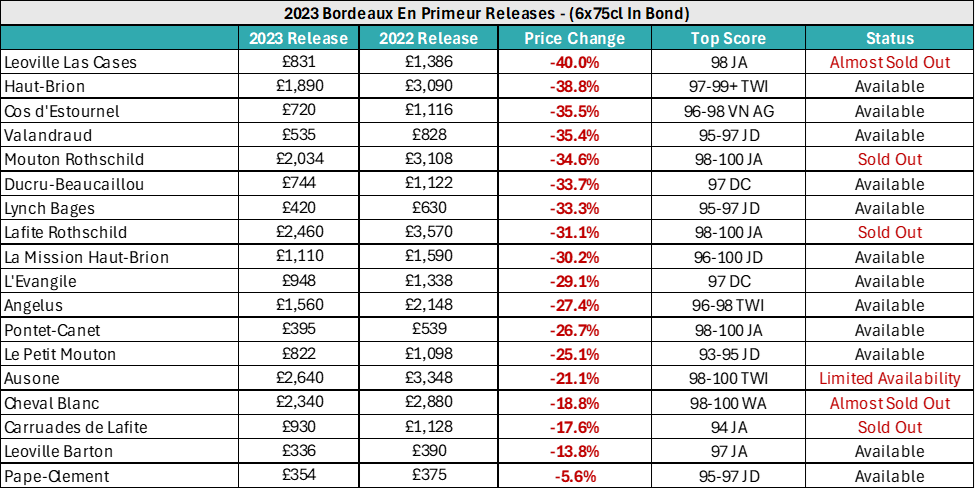

Looking at the major releases of 2023 thus far, there is no question that most châteaux have responded seriously to the altered market conditions of the last 18 months. The average price change of 2023 release prices compared to 2022 stands at -27.7%, with a number of releases seeing discounts of more than -30%:

We haven't seen year-on-year price reductions like these since the 2019 vintage was released into the gale of the Covid panic of 2020. But in 2020 financial markets were collapsing - people feared mass mortality, depression and even civilisational breakdown. Right now, (many) financial markets are at all-time highs, and retail sales are far from recessionary levels.

A mythology has grown up around the so-called 'price slashing' of the 2019 vintage. In reality, what we are witnessing this year puts 2019 into the shade. Using Léoville-Las Cases 2023 as an example: the price reduction this year was -40% below the previous vintage, whereas the reduction of the 2019 over the previous 2018 price was only -19.6%. This year Lafite Rothschild 2023 was reduced by -31.1% whilst the 2019 price drop was only -14.8%. And so on...

In fact, we have to go back all the way to the 2011 vintage (which followed the post 2009/10 collapse in Chinese demand) to find year-on-year price reductions of anything like the magnitude we are seeing this year. This surely confirms that most Bordeaux properties, and the community of negociants etc. that support them, are in earnest when they say they believe in the en primeur system and want to ensure its survival, and indeed health, into the future.

Collector demand is still there - if the price is right

2023 has confirmed that fine wine collectors have certainly not fallen out of love with en primeur.

The right wine, at the right price, is still meeting robust demand, as evidenced by the number of releases that are either SOLD OUT, or soon will be: Lafite Rothschild, Mouton Rothschild, Carruades de Lafite, Cheval Blanc and even Léoville Las Cases. We have a number of releases where sales (at least in unit terms) are well above what we sold in 2022. And even more encouragingly, the percentage of our total sales which have gone to clients in Asia is significantly up on last year.

Collectors are still bought in to the concept of en primeur. It still resonates as an exciting process that many collectors want to be part of. And as long as their loyalty and trust isn't abused, collectors will be there to support their favourite châteaux.

Back vintage pricing cannot be ignored

There has always been a resistance (at least in some quarters) in Bordeaux to recognise that back vintage pricing matters for new release pricing (or at least for new release selling!). To those of us who have been involved markets, this has always been baffling; but one clear lesson from 2023 is that châteaux who ignored where comparable vintages of their wine could be bought in the secondary market did so at their peril.

Releases like Lafite Rothschild and Mouton Rothschild 2023 (amongst others) worked well this year because, at release price, you couldn't buy a comparable back vintage cheaper. It sounds so simple, but the concept still hasn't been grasped by everyone. But it is starting to be. The reality is that châteaux have a choice: if they don't like where their back vintages are trading, they have the opportunity to put their balance sheets to work to buy them up, creating the upwards sloping 'curve' that will make their new releases irresistible.

But if they don't, they cannot be surprised if collectors turn to the back vintage market instead, as we have seen on more than one occasion during this campaign.

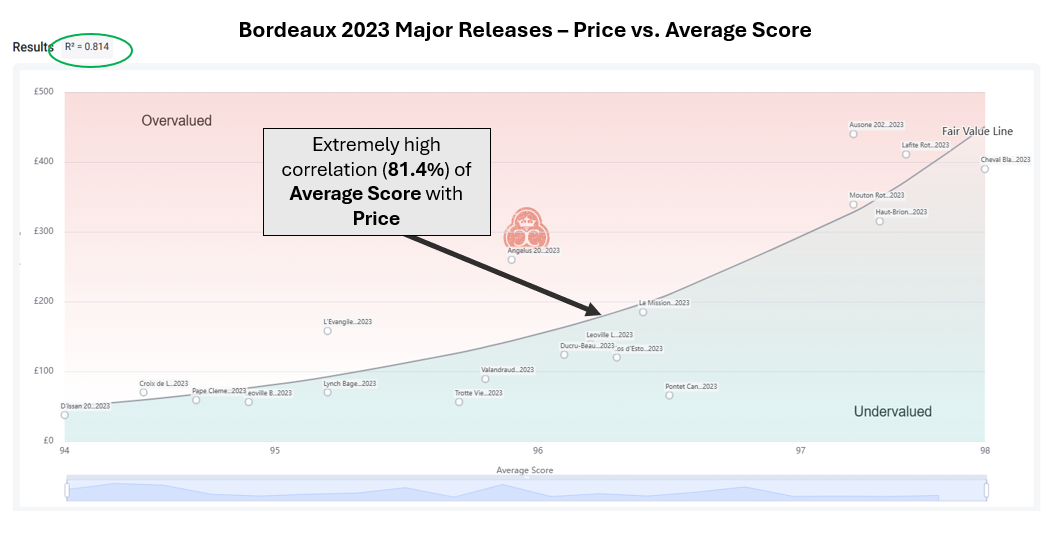

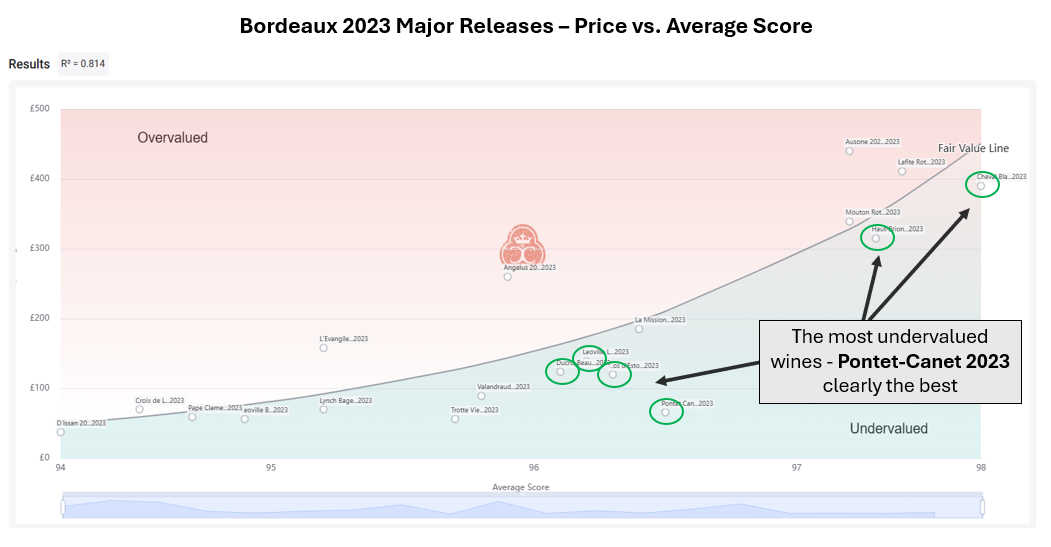

Score is a much bigger determinant of price than people realise

Received wisdom has it that classification and château reputation matter most when it comes to Bordeaux prices. But the data doesn't support this view. In fact, once you adjust for the vagaries of critic variability by using average critic score, you find a staggering high 81.4% correlation of between score and price in Bordeaux 2023:

Only a handful of wines (Angelus and L'Evangile on the 'overvalued' side, and Pontet-Canet on the 'undervalued' side) deviate very far from the 'fair value' line. Wines like Cheval Blanc and Lafite Rothschild are the most expensive of the campaign because they have the highest average score. Of course, this analysis will be challenged a bit when we get releases from Petrus and Le Pin, but generally speaking, the market has got more and more efficient over the past decade, with average score now explaining 4/5th of pricing.

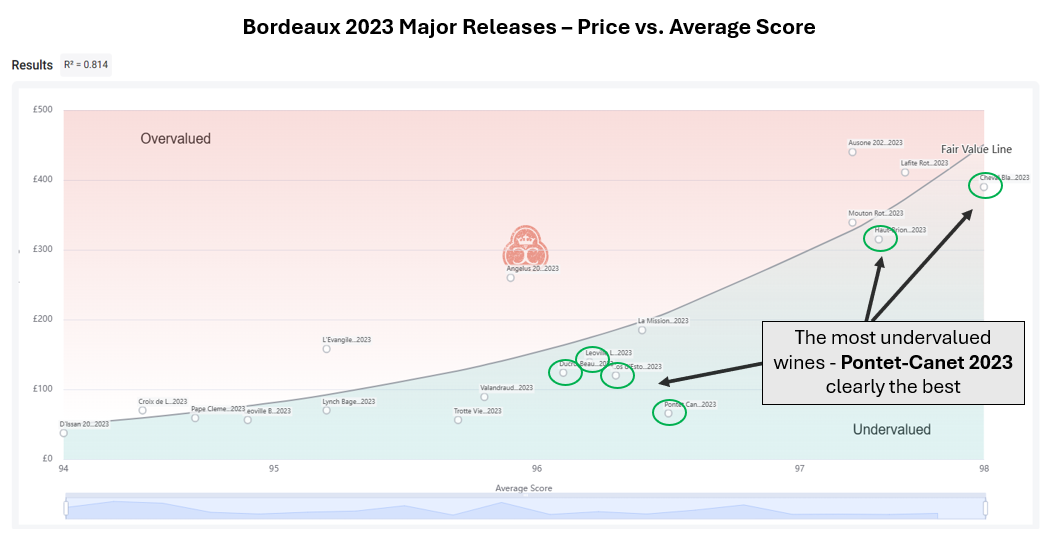

'Best Buys' from the campaign so far

Given how closely price tracks average score, there is no need to 'over think' which 2023 wines are the most attractive. You can just read them off our graphic - which you can re-create for free on this screen: here.

Pontet-Canet 2023 is head and shoulders above the pack in terms of undervaluation, which goes a long way to explaining its popularity in the campaign so far. The fact that it isn't sold out yet merely reflects that it is a pretty big estate, and the campaign hasn't been going that long! Any collector who hasn't bought a box of this needs to ask themselves why not.

But other wines which are undervalued on a theoretical basis include Ducru-Beaucaillou 2023, Léoville-Las Cases 2023 and Cos d'Estournel 2023 in the middle tier, and Cheval Blanc 2023 and Haut-Brion 2023 are also still available below 'fair value'.

We will see what the rest of the campaign brings, but it would be surprisingly if it wasn't more of the same - with most châteaux pricing their wines to offer a genuine discount and clear incentive to buy en primeur.

If so, then 2023 might be remembered as the vintage in which Bordeaux stared into the void but stepped back by doing (just) enough to keep the slightly odd, but ultimately very successful, process that we call 'en primeur' alive and relevant for a few more vintages to come!

Start to Fall – What Does this Mean for Fine Wine?")