The past five years have taught us some important lessons about the relationship between interest rates and luxury collectable prices.

In a nutshell: falling / low interest rates appear to have more power to drive prices upwards than we previously realised. But conversely, rising / high rates can also erase those gains.

In this short note we look at: i) what happened to Fine Wine prices and Interest Rates during the period 2019 - 2024 when interest rate first fell, and then rose, dramatically; and then ask ii) what will happen to Fine Wine prices over the coming easing cycle - which began in September 2024.

Easing Cycle: Jul 2019 – Feb 2022 | Plummeting Rates send Fine Wine Prices Skywards

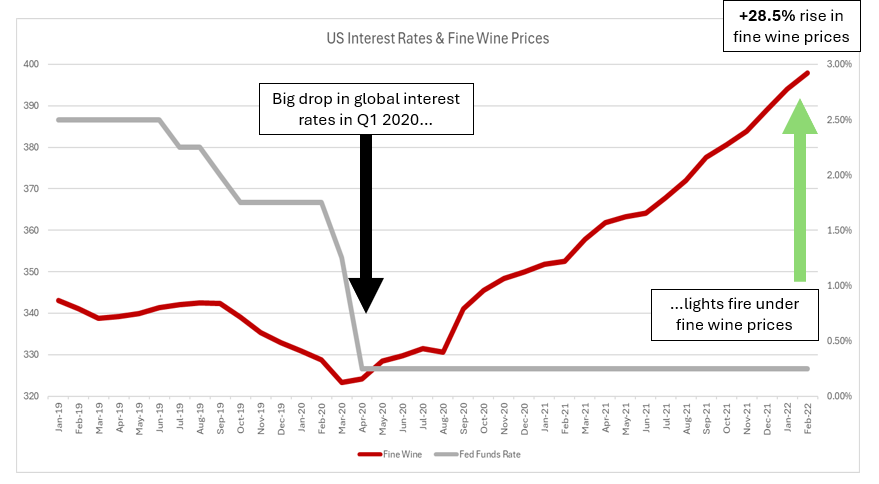

When Covid-19 panic hit markets in Q1 2020, global interest rates fell precipitously. US rates fell to a historic low of just 0.25% by April 2020. Interest rates in most industrial economies (inc. China) followed a similar pattern. Rates then remained at their ultra-low level for almost two years.

Fine Wine prices started to take off in right as global rates troughed (in March 2020). Between March 2020 and September 2022 Fine Wine rose +28.5% in one of the steepest short-term gains in history. The correlation between falling / low interest rates and rising fine wine prices is unmistakable:

Source: Bloomberg and Liv-ex.com

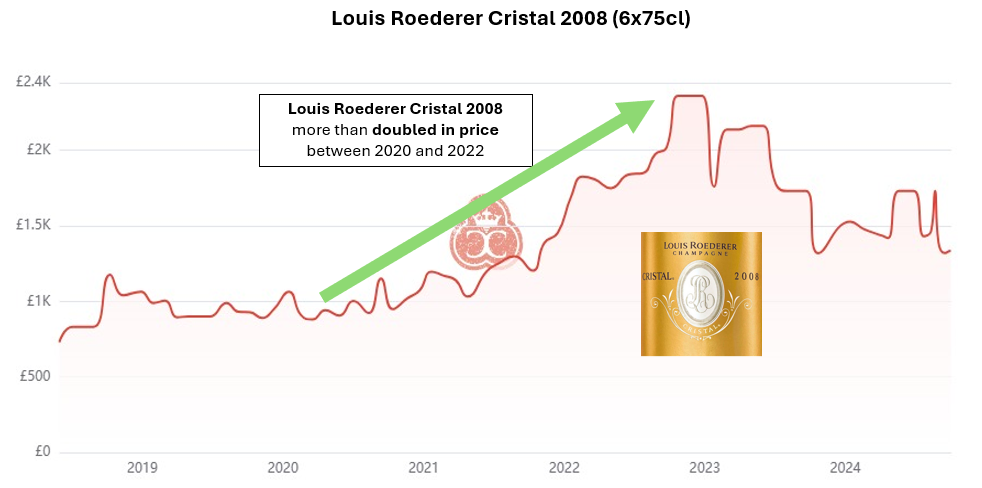

The graphic above refers only to the broad Fine Wine index. Many individual wines did far better over this period. Louis Roederer’s Cristal 2008 (6x75cl), for example, was trading around £1,000 per case in March 2020. But by the peak of the market in September 2022 had more than doubled to over £2,000 per case!

Other top Champagnes and top red Burgundies saw similar (or even greater) gains over this period.

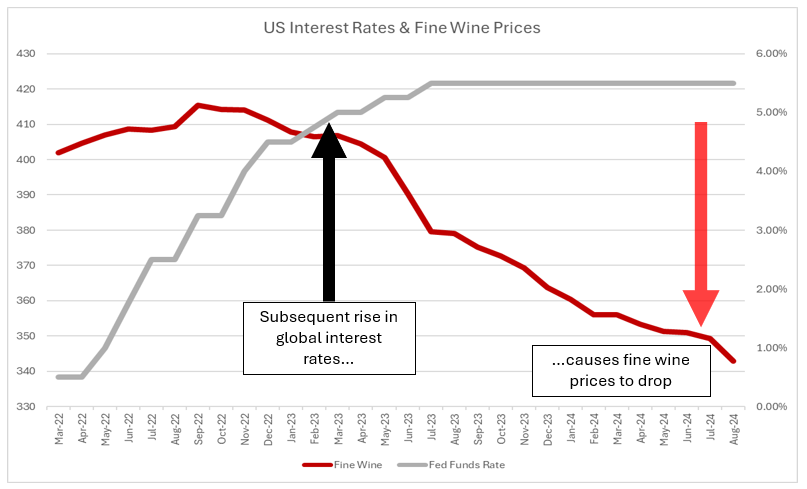

Tightening Cycle: March 2022 – September 2024 | Rising Rates put Fine Wine Prices into Reverse

With inflation rising around the world by 2022, central banks began to act. The US Federal Reserve finally started to lift US interest rates in March 2022. From the low of 0.25%, rates rose dramatically up to 5.5% by July 2023. The effect on Fine Wine prices wasn't instantaneous. Prices continued to rise for another six months after the first rate hike (i.e. until September 2022) before they went into reverse. For the next two years (until today) they have been declining steadily, down -17.4% from peak to today:

Source: Bloomberg and Liv-ex.com

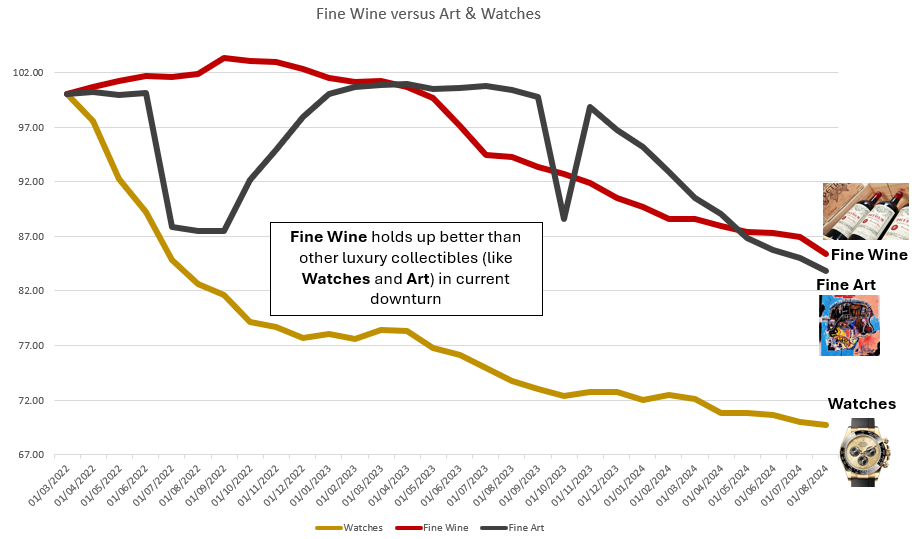

Fine Wine was not alone in being undermined by rising global interest rates. In fact, wine performed better than most other luxury collectables. Since the first rise in US rates in March 2022, the Rolex Watch index, for example, is down around -30% - almost twice as much as Fine Wine. Fine Art also performed worse than Fine Wine over this period.

Source: WatchCharts.com, Art Market Research and Liv-ex.com

Why do Fine Wine Prices Fall when Interest Rates Rise?

The answer is twofold: i) the opportunity cost of holding zero-yield assets increases and ii) expectations for future inflation decreases when interest rates rise.

When interest rates are very low (as in 2020-2022), the difference between the yield on bank deposits and that of assets which produce no yield (Fine Wine, Gold, Silver, Bitcoin, Watches, Art etc.) is very low. There is almost no 'opportunity cost' to holding the latter. But as rates rise, holders of luxury collectables must give up more and more in 'lost interest'. They therefore sell zero yielding assets and put the capital into higher yielding investments.

In addition, rising interest rates curtail economic activity, causing expectations for future inflation decline and 'fixed supply' assets like Fine Wine, Gold, Silver, Bitcoin etc. - which hedge against inflation - become less attractive.

But of course, the converse is also true. As interest rates come down, it becomes more attractive to hold assets which offer no yield. And as economic activity picks up, inflation expectations rise and inflation hedge assets like Fine Wine become more attractive.

New Easing Cycle: September 2024 | What Does it Mean for Fine Wine?

The US Federal Reserve finally began its new easing cycle with a 50bps cut in rates in September 2024. Other central banks like the Bank of England (August 2024) and European Central Bank (June 2024) had already kick-started their easing cycles months earlier. The Bank of China - which had started cutting Renminbi rates way back in 2019 - never raised rates at all and has continued cutting steadily (most recently in July 2024).

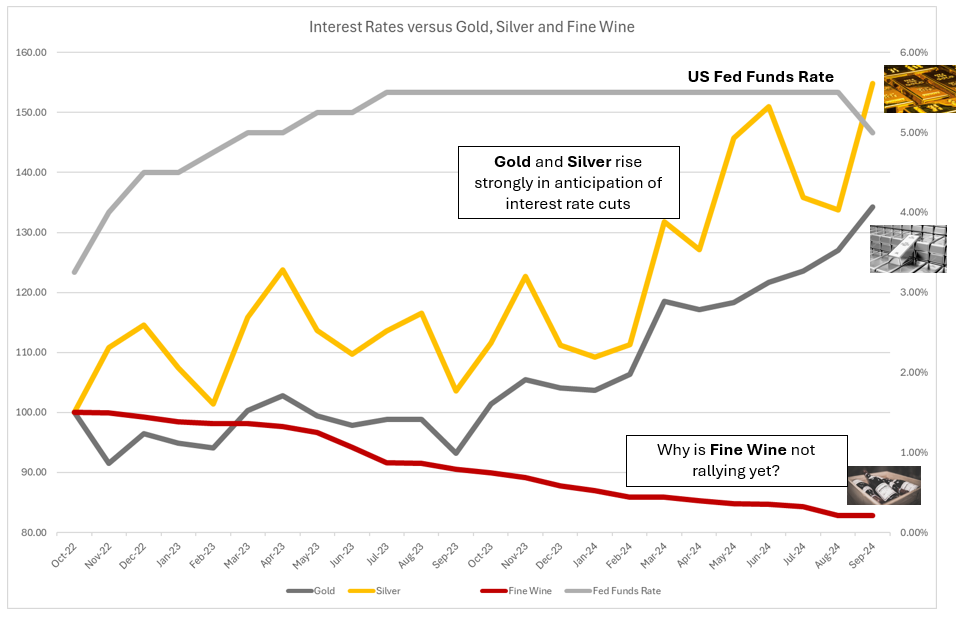

Some zero yielding / inflation hedge assets (like Gold, Silver and Bitcoin) have already risen strongly, anticipating the current easing cycle which is now priced into global interest rates.

Source: Bloomberg and Liv-ex.com

Why hasn't Fine Wine joined the party yet?

The answer lies in market structure. Although they do have industrial use cases, short-term movements in Gold and Silver (and certainly Bitcoin) are determined mainly by speculative flows, which anticipate financial conditions in the future. These markets are much quicker to anticipate changes in liquidity (i.e. interest rates and money supply) than markets like luxury collectables. But as we have seen with the last easing cycle (2020-22), eventually easier monetary conditions will find their way into all luxury collectable markets, including Fine Wine.

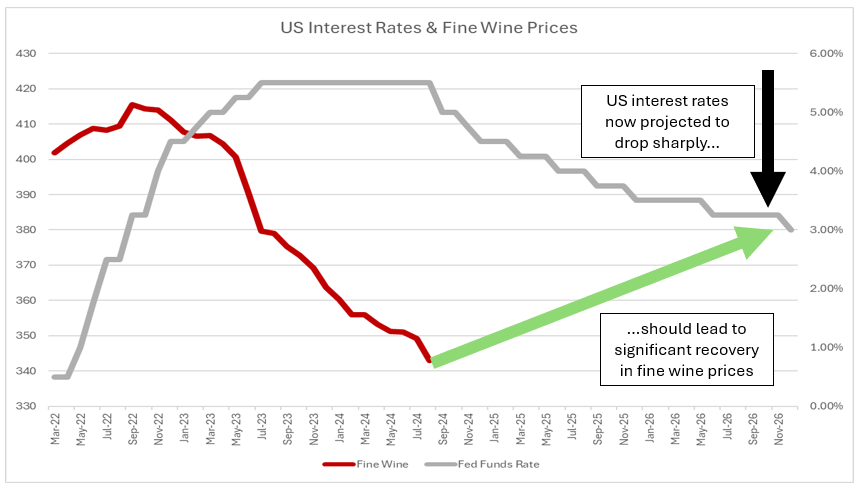

Bond markets are currently pricing in quite steep declines in most major economy interest rates over the next year and a half. US interest rates are projected to fall from their high of 5.5% to a low of 3.0% by December 2026. As these rate cuts move from 'projection' to 'reality' it seems inevitable that assets like Fine Wine will start trending upwards and catch up with commodities, precious metals and Bitcoin.

Source: Bloomberg and Liv-ex.com

What Should Fine Wine Collectors Do?

The current downturn in Fine Wine prices is now two years old, which is long for a market correction in our space. Value is starting to emerge in a number of areas. Primary market (i.e. new release) pricing hasn't yet caught up fully to the new market environment, and so collectors should focus their attention on back vintages from top years which are available at or close to recent release prices. This is the case for a number of top wines from Bordeaux, Napa Valley and (to a lesser extent) Burgundy and Champagne.

We will be publishing a series of 'Buy List' recommendations over the course of October, and we urge all collectors to prepare now for what should be a 'once in a cycle' buying opportunity as the interest rate easing cycle gathers pace through the Autumn and into 2025.

Jeremy Howard

Cru World Wine Co-Founder and CEO

jeremy.howard@cruworldwine.com