Financial Markets in Turmoil in 2022

In 2022, a surge in global inflation has wrought havoc with the world’s financial markets. From their Q4 2021 highs, global equities and bonds are both down -14% (MSCI World Index and JP Morgan US$ Corporate Bond Index — as of 31st May 2022).

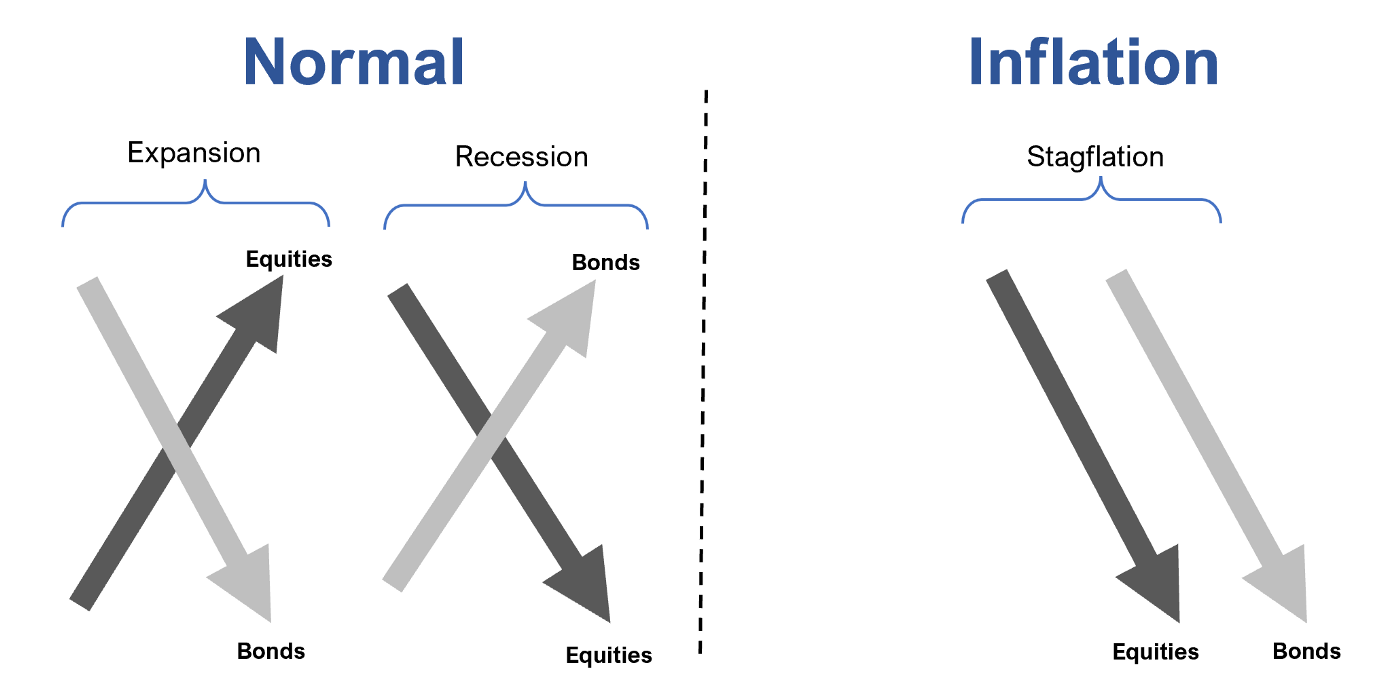

Even more importantly, the fundamental ‘laws’ of financial physics are being challenged. For 40 years, the backdrop of low and falling inflation meant that investors could rely on the inverse relationship between bonds and equities. In recessionary periods, equities fell but bonds rose, providing a natural hedge — and vice versa.

But as we move into a period of sustained inflation, this hugely valuable inverse relationship is breaking down. Bonds can no longer be relied upon to hedge equities, and the traditional 60% Equities / 40% Bonds portfolio is ceasing to produce positive returns.

Many investors and commentators are suggesting that the 2020s might require a total rethink of portfolio allocation strategy.

Inflationary Times Demand New Rules

In a highly influential paper, hedge fund Man Group plc and Duke University looked at the impact of sustained inflation on investment returns. Their report makes for grim reading for traditional asset classes.

Drawing on almost a century of data for the United States, United Kingdom, and Japan, the research showed that equities and bonds both perform poorly during inflationary times. The annualized real return of U.S. stocks averaged -7% during the eight inflationary periods since 1945. Real estate was no better, also falling (in real terms) during bouts of inflation.

The only two asset classes which reliably outperformed in inflationary times were commodities and collectables.

Source: Bloomberg report of Man Group plc and Duke University

The Man/Duke study found that collectables such as art, fine wine and stamps performed especially well during inflationary periods, with real annual returns of between +5% and +9%.

For this reason, some financial commentators have labelled this present decade the “Tangible 20s” — meaning the 2020s will favour ‘hard’ assets such as oil, gold, agricultural commodities and collectables.

Fine Wine Decouples from Equities and Bonds

The findings of the Man Group / Duke report echo our own research into Fine Wine price movement...

Since it became clear that global inflation wasn’t just a temporary phenomenon late in 2021, there has been a marked divergence between Fine Wine performance and that of bonds and equities:

Source: Liv-ex.com and Bloomberg

Fine Wine has, as in the past, decoupled from equities and bonds and is clearly outperforming in an inflationary environment.

Fine Wine Outperforms over a Quarter of a Century

Fine Wine’s lack of correlation with mainstream assets has actually been demonstrated over a very long period.

Since 1988 Fine Wine has outperformed all major asset classes by a significant distance:

Source: Liv-ex.com and Bloomberg

Fine Wine’s compound annual growth rate of +14.3% over the last quarter of a century is quite remarkable:

Low Volatility and High Sharpe Ratio

Fine Wine has also been much less volatile than most mainstream assets. This reduced volatility has given it an excellent Sharpe Ratio (which measures ‘risk adjusted’ returns). Fine Wines’ ‘risk-adjusted’ return is better than any other mainstream asset, bar U.S. Treasuries, since 1988.

Fine Wine has exhibited ‘equity-like’ returns with ‘bond-like’ volatility for the last quarter of a century!

Lack of Correlation with Mainstream Assets

The third key benefit that Fine Wine can offer is portfolio diversification.

Over the past 25 years, Fine Wine has been almost completely uncorrelated with mainstream assets:

Source: Liv-ex.com and Bloomberg

This lack of correlation means that Fine Wine can be added to any investment portfolio and will raise its risk-adjusted return. This is the ‘holy grail’ of portfolio construction.

Conclusion

If the 2020s are indeed going to be “Tangible 20s”, then we believe that all investors should consider allocating part of their ‘tangible’ position to Fine Wine.

This underappreciated alternative asset class offers a highly impressive ‘CV’ of achievements over a long period:

- Exceptionally good absolute returns.

- Extremely low volatility / High Sharpe Ratio.

- Almost completely uncorrelated to mainstream assets.

Start to Fall – What Does this Mean for Fine Wine?")